Last fortnight, CaratLane reported yet another profitable quarter, becoming the fastest-growing subsidiary of Titan.

An Affair with Gold

Mithun Sacheti was watching the world transform

In 2007, Apple released the first iPhone, which quickly became a sensation with its sleek design and touch screen. People everywhere were upgrading from their old flip phones.

Meanwhile, in India, e-commerce companies were starting, hoping to change the unorganised market. A little bookstore called Flipkart started. Despite all this progress, e-commerce companies were not focusing on something essential to Indians – selling gold accessories.

Mithun came from a family with a rich history in the jewellery business. His family owned Jaipur Gems, an Indian jewellery company, for over five decades.

Mithun grew up in the business and learned the industry’s nuances from a young age. He studied at the Gemological Institute of America (GIA) in New York, where he learned about the technical aspects of the jewellery business.

After his graduate studies, Mithun joined the family business but wanted to try something different.

In 2008, he had a Eureka moment while running his jewellery store, Jaipur Gems. As he watched customers fawn over expensive solitaires, he realised that he could sell these without actually carrying any inventory.

It was like magic, except he had a laptop and an internet connection instead of a wand.

Who needs a brick-and-mortar store when you can sell jewellery from the comfort of your couch while wearing sweatpants? It was the ultimate dream come true for entrepreneurs.

Sacheti wanted to focus on the discovery by building an online jewellery business, effectively disrupting the existing retail business model. He was hacking through the jungle of traditional retail to bring his customers the treasure trove of fine jewellery they deserved.

He saw the potential, but to make this happen, Sacheti needed help from a tech co-founder to build an e-commerce business.

Enter Srinivasa Gopalan

The duo founded CaratLane in 2008 and launched an e-commerce platform in 2010.

Marrying with Diamonds

Sacheti was a man on a mission.

After speaking to dozens of women across the country, to understand nuances, he discovered a crazy paradox.

Indian women loved jewellery, but most kept it in bank lockers where it was safe. It was unwearable every day because the designs needed to be updated. They had sports cars that they could not drive.

Sacheti figured that the contemporary Indian woman no longer wore jewellery to look beautiful or elicit compliments. Women appreciated beautiful jewellery that drew out their compelling individuality and made them feel good rather than look good.

55% of the demand for jewellery in India was thus for everyday use.

This was the problem even a large store or a chain of stores could not address because of inventory issues. He also understood that these women were savvy; they based their decisions on knowledge and access to information.

With CaratLane, the problem was addressed. Founders knew that in the age of the internet, online shopping was the way to go.

Despite being an online jewellery business, the founders realised that a gap in their customer experience still needed to be filled. While their online platform allowed for a great deal of convenience, some customers still preferred to see and touch the jewellery before making a purchase.

In 2011, they decided to open CaratLane’s first physical store in GK Delhi, becoming the first-ever omnichannel jewellery brand. A physical presence was significant given the market’s fake and low-quality jewellery prevalence.

Early in the business, CaratLane figured that gold jewellery would be low-margin. Gold was heavily regulated in the Indian market.

It was time for a strategic decision.

CaratLane decided to focus on diamond jewellery over gold jewellery. Diamond jewellery has higher margins and can be marketed as a luxury item representing status and prestige.

Traditional independent jewellers make most acting as money lenders by offering loans against gold jewellery and charging an annual interest of 18-30%. Unlike banks and non-banking financial corporations where loan-to-value is 75%, as stipulated by the RBI, the LTV for jewellers is about 60-70%, offering them a better margin of safety.

Sacheti wasn’t interested in this business model.

The cost of gold was also transparent and known to everyone, leaving little room to play with margins. The only way to make money in the gold retail segment is to scale up the business and earn via higher making charges.

But diamonds were different. They have not determined how much they cost and traditionally had better margins.

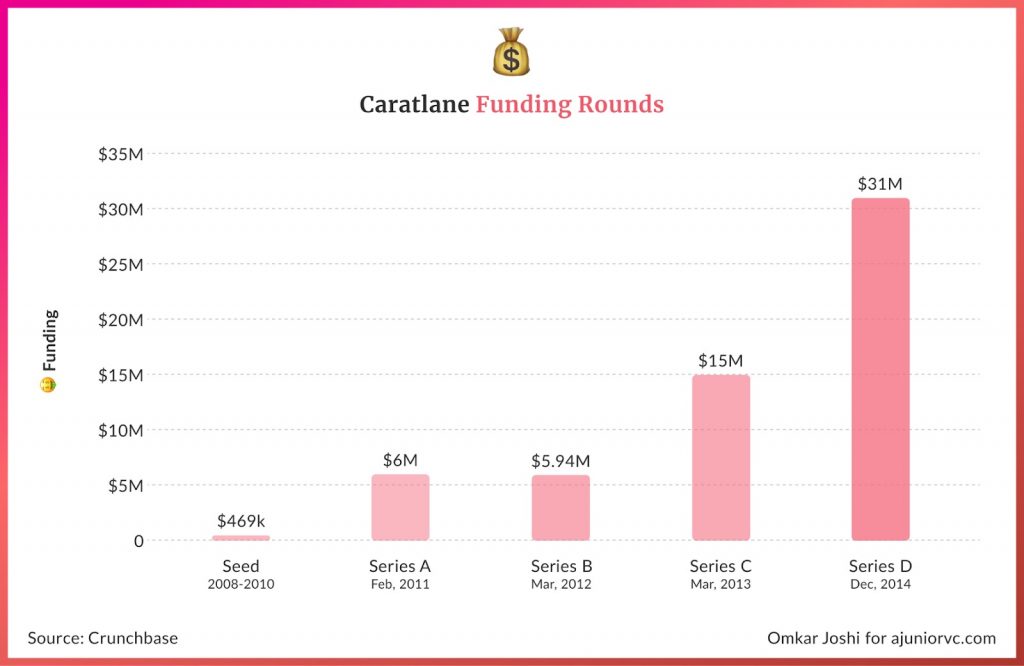

Focusing on diamonds rather than gold, they could offer their customers high-quality jewellery at a lower price. The idea was right, and capital followed them raised a $6M Series A in 2011.

Young Indians were looking for jewellery that was not only beautiful but also unique, reflective of their style and affordable. By focusing on diamond jewellery, CaratLane was able to differentiate itself from traditional jewellers who primarily offered gold jewellery.

As a result, CaratLane posted a solid revenue growth of 300% compared to 2011.

In 2013, CaratLane announced that its annual revenue had reached $25M. This represented a significant increase from the previous year, owing to new product categories, the launching a mobile app and a virtual try-on feature.

Investors trusted the decision, and soon CaratLane could raise $6M Series B in 2012 and another round in a year, $15M Series C in 2013.

David was ready to compete with the Goliaths.

Competition is Forever

As India’s internet ecosystem was taking off, so was CaratLane.

With the funding, CaratLane invested in technology, including its mobile platform. CaratLane launched the world’s first virtual jewellery try-on app, Perfect Look, to provide customers a more immersive and engaging shopping experience.

At the same time, it was important to expand the physical footprint.

CaratLane continued to expand, opening new stores in cities such as Mumbai, Bangalore, and Delhi. By 2014, CaratLane had 12 offline stores with 20 more in the pipeline.

In 2014, CaratLane reported achieving a gross merchandise value (GMV) of $50M. This represented a doubling of its GMV from the previous year.

To continue to power its growth, CaratLane Raised $31M Series D in 2014. It was one of the largest fundraisers for what was a D2C brand, even before D2C was a thing.

With the capital, CaratLane decided to focus on expanding distribution and logistics.

In 2015, CaratLane partnered with Amazon to expand its reach and customer base in India. CaratLane wanted to nail the market.

There was competition too.

BlueStone and Voylla expanded its product offerings, launching several new collections, including bridal, ethnic and contemporary jewellery along with diamond solitaires, during this period.

Feeling the heat, CaratLane introduced same-day delivery to differentiate itself in India’s competitive online jewellery market.

The move was also in response to the growing demand for faster shipping options in the e-commerce industry. With major players like Amazon and Flipkart offering fast and reliable delivery options, CaratLane recognised the need to stay competitive.

CaratLane was on the growth path, but the entire e-commerce industry faced challenges towards the end of 2016.

One major factor was a slowdown in the overall economy, which affected investor confidence and made it harder for companies to secure funding. At the same time, many e-commerce companies were burning through cash to acquire customers and build out their infrastructure, which led to concerns about their long-term profitability.

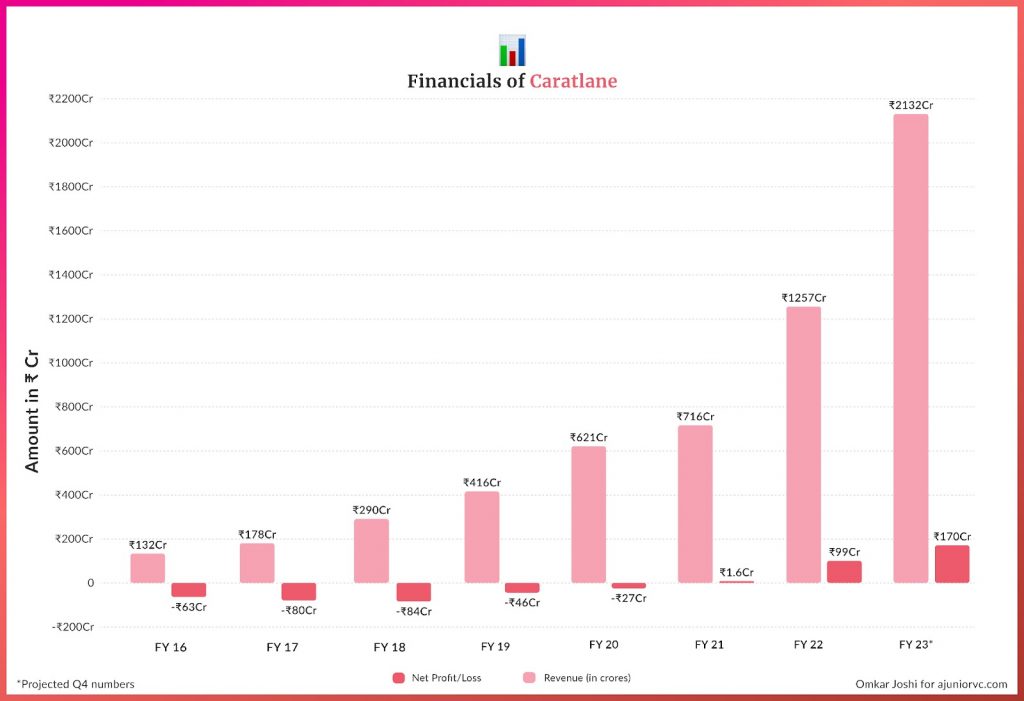

CaratLane reported a loss of Rs. 63 crores in FY2016, despite generating revenue of Rs. 141 crores.

Despite CaratLane’s innovative approach and early success, the company faced significant challenges in India’s rapidly changing e-commerce industry.

It wanted to go offline and open stores, but its big investor didn’t agree.

Diamond Dropped Like Worthless Rock

CaratLane needed firepower to grow its business

CaratLane needed to go offline.

Tiger, which was CaratLane’s largest shareholder, was also fighting fires at Flipkart, its blue-eyed boy. The founders at CaratLane wanted to go offline, while Lee Fixel at Tiger didn’t agree with the strategy.

Tiger and CaratLane felt doing what was best for the business was right, as the founders believed the store route was the best. The board decided to look for a strategic who could help with store expansion, with Tiger reducing some stake.

Enter Titan, whom CaratLane had been in touch with since 2011 as a business partner. Tiger initially offered to give up 25% of its ownership. But Titan wanted majority, or wouldn’t come in.

Titan eventually acquired 65% stake in the company in May 2016 Titan acquired 65% of the company for $50M, the same value as was deployed in the company over 3-4 years.

In 2014 the online jewellery market was estimated to be a meagre $153M (0.4%) compared to the overall Indian retail jewellery market of $38B.

While Indians took baby steps to adopt e-commerce, many hesitated to make high-value jewellery purchases exclusively online. They were sure of the quality once they physically checked the products.

Participation in the formal banking systems also posed a challenge for potential /customers.

BlueStore and CaratLane had to fight an uphill battle to gain consumer confidence by offering a wider range than physical stores and winning the trust by offering customers an option to try the shortlisted jewellery at home.

Online jewellers weren’t targeting the mother with her high-value purchases anymore, but rather the working daughter’s discretionary spending. This meant they were competing for the same share of wallet as consumer electronic gadgets, apparel or accessories.

While the Average Selling Price (ASP) for the offline jeweller Tanishq was ₹ 90,000, CaratLane’s was ₹25,000.

Troubled by the model not working, CaratLane gave an exit to its investors, with the founders staying on.

The story of building a unicorn appeared to be finished for Mithun

Shine on You Crazy Prices

In their new role as a founder of a Titan subsidiary, Mithun got to business

The Indian retail jewellery market had grown immensely at a CAGR of 14% from 2014, reaching an estimated $64B by 2017.

This growth of the Indian jewellery industry could be attributed to various factors, including the increasing disposable income and changing fashion trends where jewellery was now bought for work, especially among younger girls. While women have traditionally dominated the jewellery industry, men make up almost 10% of all purchases.

Consumers had remained loyal to their family jewellers, resulting in a large presence of community-centric jewellers focused on relationship-building selling.

Like most other categories of the Indian retail sector, the jewellery industry too was dominated by small and medium-sized enterprises where organised entities such as Tanishq, PC Jewellers, and Kalyan Jewellers made up only 30% of the market.

However, with increased digital exposure, the rise of nuclear families and increased receptiveness to buy online, including expensive white goods, these traditional linkages were growing weaker

Organised players could find an in.

CaratLane beat these typical retailers at exactly that

They reached almost 0 by establishing a robust network of 4,000 diamond vendors across India, Hong Kong, Israel, New York and Antwerp.

Then they avoided the common retail challenges by owning their entire manufacturing setup and keeping their product range simple and modern. They deployed the Dell model, where the manufacturing began only once the order was placed.

They also operated with a virtual storefront to save costs on rental and operational expenses, resulting in significant savings compared to traditional brick-and-mortar jewellers. These gave them about 34% savings compared to their high-street counterparts.

This meant CaratLane could price their products much lower, similar to the strategy adopted by Blue Nile, the pioneers of the online jewellery market in the US during the early 2000s.

CaratLane’s largest stakeholder and India’s largest jewellery retailer, Tanishq, across its 320 stores, reported revenue of $ 2.4B in 2018 with a gross profit margin of 15% and EBITDA of 6% with $ 400M in operating expenses.

During the same time, CaratLane expanded its revenue to $41M with a healthy gross profit margin of 23% with $ 20M in operating expenses, owing to its expansion along the omnichannel route.

Sacheti was looking to expand CaratLane’s portfolio.

Based on customer feedback and purchase patterns, they realised people were open to buying silver jewellery, but the options were fairly generic or too expensive.

Sacheti had struck silver, a gap in the market, the sub ₹10K price range. This was a natural progression for the brand, as lower ticket items would fit perfectly for the online market.

In 2018, CaratLane decided to make inroads into the silver market.

At the time, India’s silver jewellery market was estimated to grow by 30-35% CAGR for the next 3 to 5 years. ‘Shaya’, an affordable online-only silver jewellery sub-brand under the banner of CaratLane, was born

Sacheti expected the average bill value of this brand to be less than ₹5,000, but he knew if he won the trust of this segment of customers, he could upsell to them in the future.

Like the company’s tagline, Caratlane was here to serve the customers forever.

Standing on the Shoulder of Diamonds

In 2019, Titan’s distressed acquisition was finally starting to show colour

For Titan, the thesis was straightforward. Build muscle in the nascent e-commerce jewellery space, get a team whose DNA is different than theirs and most importantly, cater to younger customers by selling at a lower price point —between Rs 8,000-10,000—something it could not do with Tanishq.

On the other hand, CaratLane had much to gain from the acquisition, especially as it was left to fend for itself.

One of the early changes was endorsing CaratLane as a Tanishq brand and leveraging Tanishq’s brand. Within six months, CaratLane branding had been prefixed with ‘A Tanishq Partnership’

Secondly, synergy benefits in sourcing, designing and manufacturing at scale were evident, and it did help CaratLane to reduce its costs further. COGS as a % of sales reduced from 83% in FY17 to 81% in FY19 to 70% in FY20.

But having access to Titan’s playbook on scale brands profitably benefited CaratLane immensely.

Learning from the Titan model, CaratLane also opted to expand its network of offline stores through franchising, allowing it to grow this channel with minimal capital outlay with no upfront costs on construction or inventory.

Several of these franchisee owners also had Tanishq franchises, with many CaratLane stores close to Tanishq outlets.

The omnichannel franchise-led route was working.

While opening a CaratLane store in Faridabad didn’t impact the total number of customer sessions, but increased the conversions by 3X. About 70% of the sales were offline, but the company believes over 80-85% are online-influenced transactions.

To drive operational efficiency and excellence, CaratLane initiated an exercise to benchmark its operational cost from salaries to marketing costs with traditional business and started improving on these metrics.

Further, CaratLane undertook an exercise to optimise inventory and reduced the SKU count from a peak of 8,000 units to half of that by focussing on fast-selling SKUs.

Being backed by the Titan brand, CaratLane had access to cheaper debt, as they obtained an AA/A1 rating from the credit rating agencies. Since the acquisition, Titan has only made a further equity investment of just ₹ 100 Crore, while the rest has come through debt.

In the time span the revenue grew from 4.7x from INR 132 crore in FY16 to INR 620 crore in FY20.

What was dreamt of while signing the deal for Titan had started to unfold in reality? But the best was yet to come

My Diamonds are Shinier than Yours

Most notably were newer D2C brands like Melorra and older horse BlueStone.

Melorra, founded in 2016, also focused on gold-diamond and gemstone-focused light jewellery. BlueStone, founded shortly after CaratLane in 2011, took a similar route of both an offline and online approach to selling Gold, Diamond and Pearl Jewellery.

It also faced competition from the big traditional players like Kalyan and PC Jewellers, who, in addition to jewellery sales, also offer jewellery purchase advance schemes, gold insurance, wedding purchase planning, booking of purchases to protect against price increases, etc.

Mithun Sancheti focused on a “jobs to be done” approach to why people buy jewellery. They looked at the gift cards that customers sent with jewellery. CaratLane realised that emotions and relationships were the biggest drivers for purchase.

As a differentiator, Caratlane started focusing on relationships and events for gifting, such as Rakhi, and Diwali. This was a differentiated brand strategy from its competitors.

Mithun called his business similar to a SaaS business, focusing on customer lifecycle management. Most jewellery businesses have a very low repeat rate. An average of 4% of their customers in a given financial year would purchase from them again in the next financial year.

However, Caratlane had 25% repeat rate.

Being digital, they had the chance to use SEO and other methods to focus on keywords relating to key events in their customers’ lives and a catalogue that focused on different stages of their lives.

This meant customers would not need to look elsewhere and would create a habit of transacting with Caratlane as much as possible. This differentiated insight was one of the reasons Caratlane was able to win in the competitive market.

Further, the high repeat rate meant customer lifetime value was much higher than the cost to acquire a customer compared to its competitors.

As CaratLane scaled, a virus threatened to play spoilsport in the online diamond jewellery party.

Diamonds are Made from Pressure

The COVID pandemic and lockdowns of 2020 onwards hit growth for all jewellers,

This was true, especially in the physical locations of Caratlane’s showrooms, many of which were located in malls.

Revenue in May and June of 2020 was 23% and 85%, respectively, compared to the same months in 2019.

However, the online channel did exceptionally well once the e-commerce lockdown restrictions shipment of non-essentials were lifted.

Realising the need for a contact-free product viewing experience, CaratLane took the bold step of launching Caratlane Live. This online tool allowed customers to preview and virtually try on jewellery without stepping into a store.

Caratlane rapidly shifted to a more omnichannel strategy, and although rough patches like April – June of 2021, where stores had to shut down due to the second wave of COVID and revenue took a hit, e-commerce and festive rebounds drove revenue to new heights By June 2022, it clocked its best-ever quarter with a revenue of 483 Cr. This was a 200% growth over the same quarter last year and higher than the total revenue for FY 2019. It cited that growth was driven by its new “Borla” jewellery collection that launched during Akshaya Tritiya in April 2022.

Online searches and orders for gifting occasions of birthdays & anniversaries displayed a high organic intent for the brand.The event and relationship-focused strategy were starting to pay dividends.

It also entered the US market in 2021 and, by 2022, had delivered $1.2m of booked revenue there.

In FY 2021-2022, it earned Rs 89 crore net profit on Rs. 1,255 crores of revenue. This was impressive when we contrasted it against an industry leader like Kalyan Jewellers.

In the same period, Kalyan made a profit of 224 crores on Rs. 10,818 crores of revenue, nearly all of which came from Jewellery sales. Its profit margin was 1/3rd of CaratLane’s.

In comparison, its competitor Melorra earned Rs. 471.3 crores and lost 100 crores, and Bluestone’s revenue was Rs. 461.3 crore for a loss of 42.5 crores,

Reading the investor reports and CXO interviews, CaratLane’s outlier performance in this category could primarily be because of its omnichannel approach.

From the bleak and dark days of 2016, life had come a full circle for Caratlane, and it was at its glittering best

Expressing Emotions

CaratLane came out through the pandemic much brighter.

In Q2 FY’23, it achieved Rs. 445 Cr, representing 54% QoQ growth. Over the last two years, its 2-year CAGR has been 76%. The Indian consumer has become used to buying jewellery online, which was unthinkable even 5 years ago.

CaratLane isn’t resting on its laurels.

Taking a page from the Tata international partnership playbook, it recently announced a deal with Warner Brothers to launch Harry Potter jewellery focused on young adults and teens. With an accessible ASP of Rs. 4500 – Rs. 25,000, this will bring the next generation of Indian Jewelry consumers as CaratLane aficionados.

While CaratLane may have opened its 182nd physical store recently and now has a vast physical footprint, its DNA is still very much digital. Physical stores act as a marketing channel where customers can “walk into the stores, order online and try our jewelry at home. For example, a customer can try on a gold earring in a store and order her size online.

This is even more important in a high ASP category like jewellery

Its parent company Titan has its eyes set on the overseas market focusing on NRIs who have a cultural attachment to Indian jewellery. NRIs also tend to be affluent; for example in the US, the median household income for Indian Americans is $100K vs $70k overall. Titan has estimated this market to be $3-4Bn, representing a huge untapped market.

However, an international expansion will not be easy for CaratLane as it faces massive competition in the everyday accessible jewellery category.

Companies like Monica Vinader and Pandora dominate this market and there’s no real differentiation for CaratLane. As a result, Titan may decide to focus on selling Indian-themed jewelry through Tanishq and Zoya, and leave CaratLane to focus on India.

Not that there’s any dearth of opportunity here. The share of online jewellery in India would double in the next 5 years from 3-5% to 7-10%. Online buyers purchased lightweight daily wear in 18-carat gold – CaratLane’s sweet spot.

As the market leader, Caratlane benefited greatly from people staying in and ordering jewellery online. It’s parent company Titan often trades at a premium as more than 90% of the Indian jewellery market is still unorganised and based on family jewellers.

Titan’s investment in Caratlane helped it survive through 2016 and thrive through the pandemic.

Now, Caratlane will play a critical part in Titan’s ambitions to dominate the organised jewellery space in India, specifically the e-commerce sector.

The founder’s stake of 25% in CaratLane could be worth more than the close to zero value it was dropped for. The company now does 2,000 Cr of revenue, and at Titan’s 6x revenue, multiple could easily be worth 12,000 Cr.

That would make the founder worth 3,000Cr, or $350M. The earlier investors who sold their stakes for $45M, would now have been worth an astonishing 8,000Cr or $1Bn

A turnaround story like nothing India’s ecosystem has seen.

As Mithun explores other avenues, the next strategic step would probably be Titan acquiring his stake for cash and stock. It would be an acquisition that generated immense value for everyone involved.

CaratLane has become the crown jewel in Titan’s empire, with a tiny startup becoming a diamond.

Courtesy: A Junior VC